Car news and reviews

Latest car advice

Explore topics

How to plan a long distance drive in your electric car

Long-distance driving in an EV doesn’t have to cause a headache. From mapping out charge points, to our 10 top tips; we have you covered with this handy guide.

Black box insurance for young and new drivers 2026

Telematics ‘black box’ insurance can be a cheap car insurance option for young and inexperienced drivers. Learn more about how black box insurance works.

Provisional driving licences: how to apply, renew and change address

A provisional driving licence is the first step to starting your driving journey. Find out how to apply, renew or change your address on your provisional licence.

How to spot and avoid potential scams

Sell your car safely by learning about how to spot fake buyers, safely meet potential buyers, and use secure payment methods.

Service history when selling a car: why it matters and how it affects the value

A full service history is one of the most sought-after qualifications on a used car, but is it vital?

How to sell my electric car | 2026

From getting the right price to finding the right buyer, we're here to help you sell your electric car.

Tax your car online or at the Post Office (2026 update)

Find out how to tax your car online and in-person to be able to legally drive your car in the UK.

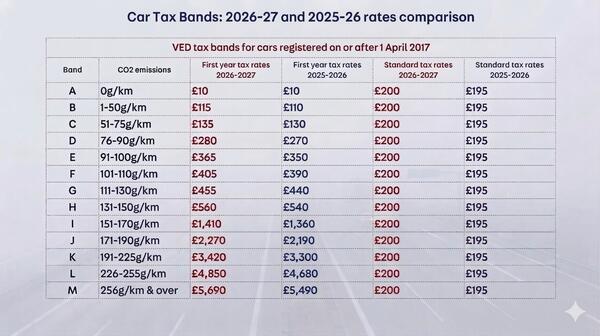

Vehicle excise duty: Car tax rates from 1 April 2026 onwards

Find out how VED tax bands work and how much tax you’ll pay for a new or used car in 2026.

How to renew car tax (vehicle excise duty)

You have to renew car tax every year to keep driving your car legally in the UK. Here we delve into different ways to do so.

Reporting potholes and the damage they cause to your car

Potholes are becoming an increasing problem in the UK: here’s how to report a pothole and how to claim compensation if a pothole has damaged your car.

MOT certificate: How to check it online

MOT certificate is an important document to legally drive in the UK. Find out how to access your certificate and download it for taxing your car.

Paperwork needed to sell a used car (2026 update)

Once the deal is done, it’s time to prepare the paperwork for selling a car. If you're wondering 'What documents do I need to sell my car', find here a list of all the documents you need to provide the buyer.